Millions face mortgage bills hike ‘of £600 per year’ as Bank raises interest rates to highest level since 2008

11 May 2023, 14:09 | Updated: 11 May 2023, 17:19

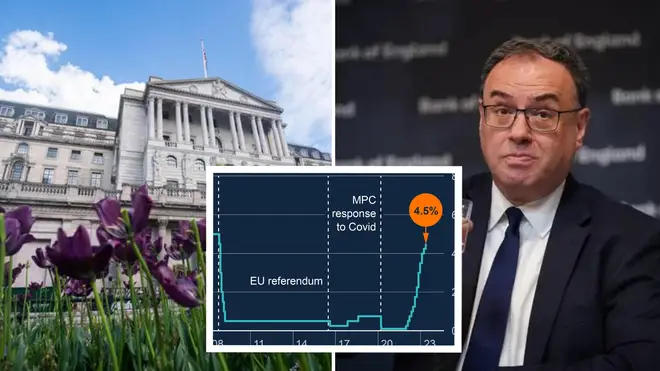

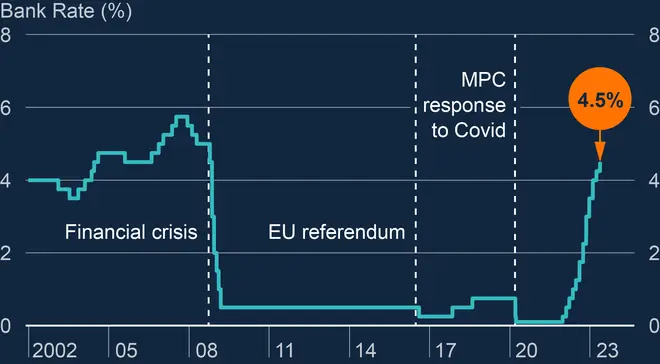

Millions of homeowners face paying several hundred pounds more each year on their mortgages after the Bank of England increased its interest rate to 4.5 per cent.

It is the 12th consecutive rise in the cost of borrowing since December 2021.

Anyone on a variable or tracker mortgage will have to instantly pay more. A homeowner with a two-year tracker mortgage of £350,000 will see their monthly payments go up by nearly £50- adding around £600 per year.

Finance expert Martin Lewis estimated a rise of £150 per year per £100,000 of mortgage loan.

He urged savers to ‘check, ditch and switch’ to make the most of bank accounts with the best interest rates, as big banks face continued criticism for failing to pass interest rate rises onto savers.

Read more: Interest rates hiked for the 11th time in a row to 4.25% as Bank of England grapples inflation surge

Speaking after the rise, Chancellor Jeremy Hunt said the Bank of England had predicted that the government was on course to meet its target of halving inflation this year, but said it was not "automatic".

Asked whether he was confident of meeting Mr Sunak's inflation target, Mr Hunt said: "The Bank of England is predicting that we will hit the inflation target.

"But there has never been anything automatic about hitting it.

"That is why it is so important, if we're going to bring certainty back to family finance, stop prices rising, that we stick to our plan to halve it."

NEWS: Bank of England base rate up 0.25% pts to 4.5% (12th consecutive rise, highest level since 2008)

— Martin Lewis (@MartinSLewis) May 11, 2023

- Variable/tracker rate repayment mortgages will rise c.£12/mth (£150/yr) per £100,000 of mortgage (use mortgage calc to check)

- Existing fixes won't change. New cheap fixed…

Some analysis has typical tracker mortgage customers paying about £417 more a month, and variable rate mortgage holders about £266 more.

The Bank of England believes the economy will avoid a recession, but does think price rises will not slow as quickly as expected due to increasing food costs.

Food inflation has been "particularly high" reaching 19.1%, Bank of England Governor Andrew Bailey said.

Borrowers on fixed mortgages will be shielded until their term comes up and they need to re-mortgage.

The Bank’s Monetary Policy Committee (MPC) said the increase was necessary to bear down on double digit inflation.

Rates are now at their highest level for 15 years, since the global financial crisis in 2008, after seven out of nine members of the Bank's monetary policy committee (MPC) voted for the increase.

The previous rate was 4.25%, after an increase of 0.25 percentage points in March. The two members who wanted to keep rates at 4.25% pointed out that inflation was already on course to fall this year.

But the Bank warned that the increase in the cost of living is expected to fall slower than previously thought.

The latest increase in interest rates is set to make life even more difficult for people on variable mortgages and some people with credit cards and overdrafts.

Some analysts believe that mortgage rates are unlikely to come down significantly for the rest of 2023.

Simon Gammon, managing partner at Knight Frank Finances, said: "The biggest conundrum for most borrowers at the moment is whether to fix for two years or take a tracker. Of course, that comes with the risk that your monthly payments will rise if the Bank of England opts to raise interest rates further, so it's a highly personal decision."

Announcing the decision to hike rates again, the Bank's MPC said there had been "repeated surprises about the resilience of demand" and that inflation had been stronger than expected as the price of food and other goods were higher amid the war in Ukraine.

The two members of the MPC who wanted to keep rates unchanged said that inflation was already expected to fall considerably this year without the need to rise the rate again.

They also said a lot of the impact of rising rates has not yet come through into the economy. The Bank estimates that around a third of the impact of rates increases has been passed through.

In a report, the committee said: "In the modal forecast conditioned on market interest rates, and taking account of stronger paths for food prices and demand growth, CPI inflation is expected to decline somewhat less rapidly compared with the February report."

Speaking about the troubles that have hit banks in recent months, committee members added: "Risks remain but, absent a further shock, there is likely to be only a small impact on GDP from the tightening of credit conditions related to recent global banking sector developments."

They said: "The committee judges that growth over much of the forecast period will be materially stronger than in the February report.

"This reflects stronger global growth, lower energy prices, the fiscal support in the spring Budget and the possibility of lower precautionary saving by households than previously thought."

Chancellor Jeremy Hunt said the interest rate rise would "obviously be very disappointing for families with mortgages.

"But unless we tackle rising prices, the cost of living crisis will only carry on - which is why we need to be resolute in sticking to our plan to halve inflation by the end of the year."

Meanwhile, economists at the Bank released a record upgrade to their economic growth expectations.

They now expect that gross domestic product (GDP) will not fall during a single quarter this year, meaning the economy is not set to decline and the UK could avoid a recession.

In February, the committee believed the economy could fall into a shallow recession starting from the first three months of the year.

The increase of 2.25 percentage points over the three-year forecast period marked the biggest upgrade since the MPC was formed in 1997.

"The improved outlook reflects stronger global growth, lower energy prices, the fiscal support in the Spring Budget, and the possibility that a tight labour market leads to lower precautionary saving by households," the report explained.

Nevertheless, higher food and energy prices will continue to disproportionally hit families on lower incomes as the items typically make up a larger share of overall spending, the Bank said.

Just two of the Bank's nine-member MPC voted to keep interest rates the same at 4.25%.