Economy set to shrink by 2% as Government debt to soar £400bn higher – OBR

17 November 2022, 16:14

The Office for Budget responsibility has said the recession is set to last ‘just over a year’.

Government debt is set to balloon £400 billion higher than previously expected, warned the fiscal watchdog as it unveiled a bleak outlook for the UK economy.

The Office for Budget Responsibility (OBR) said the economy is already in recession and will shrink further next year due to sky-high inflation.

It forecast the UK economy will be shrink by 2% in total over a lengthy recession which started earlier this year.

The OBR said squeezed incomes, higher interest rates and tumbling house prices – which it expects to drop by 9% by 2024 – are all set to contribute to a recession lasting “just over a year”.

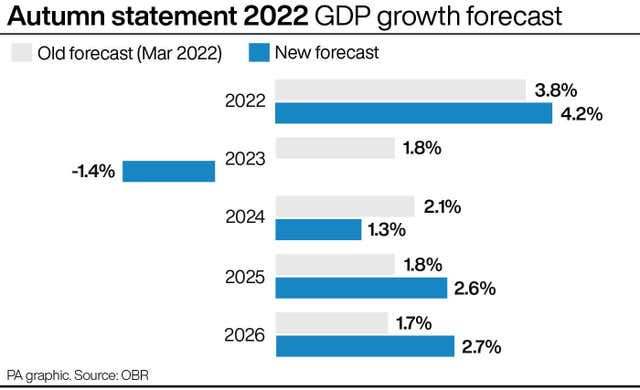

The official forecaster downgraded previous projections that the economy would actually grow by 1.8% in 2023 to a fall of 1.4% for the year.

Growth expectations for the following year were also downgraded in the face of continued inflationary pressure.

It has, however, slightly upgraded the total economic growth expected this year to 4.2% from 3.8% in the March statement.

The OBR has also predicted that inflation will hit an average rate of 9.1% this year and 7.4% in 2023.

Previously, forecasts had indicated inflation of 4% next year.

The Bank of England has repeatedly hiked interest rates during this year in an effort to drag down on inflation, with rates jumping to 3% earlier this month.

The OBR said higher interest rates has had a significant impact on Government debt, which it said is now expected to be £400 billion higher – roughly 18% of the size of UK GDP – in 2026-27 than it forecast in March.

Rate increases means that cost of servicing Government debt will double to over £120 million, which the OBR said will make public finances “more vulnerable to future shocks”.

The cost of servicing this debt will be the highest proportion since following the second world war.

Unemployment is also expected to jump over the next two years, according to the forecasts.

The rate of unemployment is set to lift from 3.6% to 4.9% in the third quarter of 2024.

Our November 2022 GDP growth forecast. Full forecast published after the Chancellor’s #AutumnStatement speech pic.twitter.com/U1iKT9KFaC

— Office for Budget Responsibility (@OBR_UK) November 17, 2022

This would mean a 505,000 increase in unemployed individuals from 1.2 million present to a peak of 1.7 million.

In his autumn statement, Chancellor Jeremy Hunt said the forecasts “confirm that our actions today help inflation to fall sharply from the middle of next year”.

“They also judge that the UK, like other countries, is now in recession,” he added.

Mr Hunt confirmed in his speech that new spending reductions and tax plans are intended to secure an extra £55 billion to help address the UK’s fiscal hole.

The hole is the extra money needed by the Government in order to meet self-imposed targets to bring down the size of state debt relative to national income.

The announcement comes a day after inflation rocketed to a 41-year-high of 11.1% in October due to surges in the cost of energy and food.

The OBR’s latest forecasts have been long awaited after the official forecasting body was not used during the September mini-budget, led by former chancellor Kwasi Kwarteng.

Economists partially linked the shock to the pound and bond yields following the mini-budget announcement to a lack of visibility on the impact of the previous government’s fiscal plan.

On Thursday, some economists questioned the outlook from the OBR, which was largely more upbeat in the medium-term than the Bank of England’s latest economic forecasts.

Martin Beck, chief economic advisor to the EY Item Club, said: “With the OBR delivering a poor prognosis for the economy’s prospects, the fiscal position is expected to face challenges accordingly, with substantial upward revisions to public borrowing over the next five years.

“But the EY Item Club thinks the OBR’s forecast is potentially too downbeat.

“The OBR’s numbers are conditioned on interest rates rising to 5%, a level which the official forecaster predicts would contribute to inflation falling below zero in 2025.

“A lower rate assumption, and one consistent with the Bank of England’s 2% inflation target, would mean a better growth outlook.”

Yael Selfin, chief economist at KPMG UK, said: “The revised set of targets outlined by the Chancellor in the autumn statement to secure markets’ confidence in the sustainability of UK public finances may not be as easily met, given that the OBR forecasts have been relatively generous.

“There is a high probability that real GDP outturn will prove lower than the OBR’s forecast, while inflation remains stickier in the short-term, adding to the Government’s expense.”