Bank raises rates to 1% and warns cost crisis will send economy into reverse

5 May 2022, 15:14

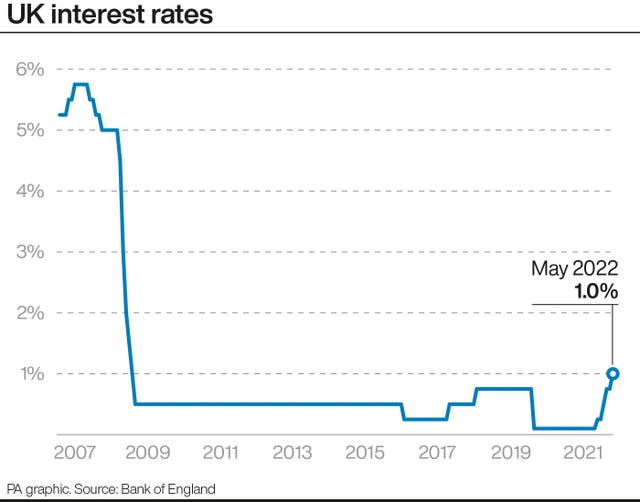

Members of the Bank’s nine-strong Monetary Policy Committee voted 6-3 to increase rates from 0.75% to 1%, the highest level for 13 years.

The Bank of England raised interest rates to 1% as it warned the economy will go into reverse and that inflation will peak at more than 10% as the Ukraine war compounds a crippling cost-of-living crisis.

Members of the Bank’s nine-strong Monetary Policy Committee voted 6-3 to increase rates from 0.75% to 1% – the fourth time in a row that they have voted for a rise – taking rates to a level not seen since 2009.

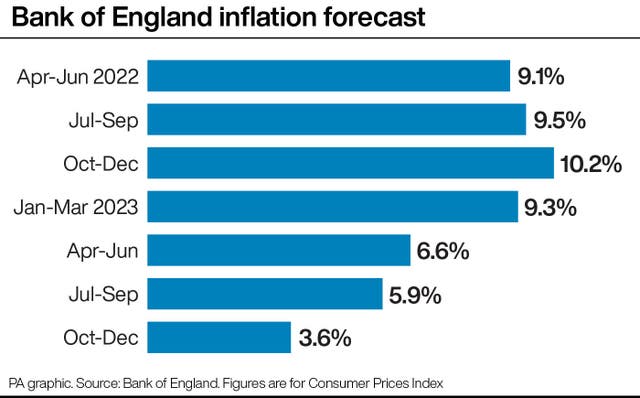

Three members called for a bigger increase to 1.25% due to worries over rocketing inflation, with the Bank ramping up its forecast for Consumer Prices Index (CPI) inflation to rise from 7% currently to more than 10% in October – its highest level for 40 years – due to soaring energy prices.

In a grim set of forecasts, the Bank predicted that growth will contract in the final three months of 2022 as the cost squeeze sees households rein in their spending.

The UK is set to narrowly miss a technical recession, as defined by two quarters in a row of falling gross domestic product (GDP).

But the Bank forecast “very weak” quarterly growth in 2023 and a contraction as a whole next year, with GDP falling by 0.25% and unemployment picking up sharply as cost pressures hit hard.

The prediction for growth in 2022 remains unchanged at 3.75%, although the Bank also slashed its growth outlook for 2024 to 0.25% from the 1% it predicted in February.

With the spectre of recession looming large, the pound fell sharply, down 0.8% against the US dollar at 1.240 and 0.9% lower against the euro at 1.174.

Sky-high inflation will see household disposable income plunge by 1.75% this year – the second highest on record, the Bank warned.

Governor Andrew Bailey said: “I recognise the hardship this will cause for many people in the UK, particularly those on the lowest incomes, often with little or no savings, who are hit hardest by increases in the prices of basic necessities like food and energy.”

He added that further rate rises are likely to be needed “in the coming months” to cool rampant inflation, but admitted that the impact on finances of soaring costs in the short term “is something monetary policy is unable to prevent”.

Financial markets predict that rates will reach 2.5% by the middle of next year as policymakers battle to contain inflation.

But the Bank signalled that rates may not rise as high as that given that this is likely to leave inflation below the 2% target at the end of its forecast.

The report makes for painful reading, with household income under severe pressure ahead of a predicted 40% hike in the energy price cap in October.

Deputy governor Ben Broadbent said the UK economy is facing a shock on a bigger scale than that seen in the 1970s oil and energy crisis, though he said it is not set to last as long.

Growth of 0.9% was better than the Bank expected in the first three months of 2022, though this looks to be the calm before the storm.

It predicts the economy will flatline in the second quarter before dropping by nearly 1% in the closing three months of 2022.

And while the rate of unemployment will ease back further to as low as 3.6%, it will jump back up to 5.5% within three years, according to the Bank.

Now that rates have hit the 1% threshold, the Bank also confirmed it will start drawing up plans for selling off some of its £847 billion in Government bonds – built up as part of its quantitative easing programme launched in 2009 amid the financial crisis.