Radical shake-up of home and motor insurance pricing proposed

22 September 2020, 12:04

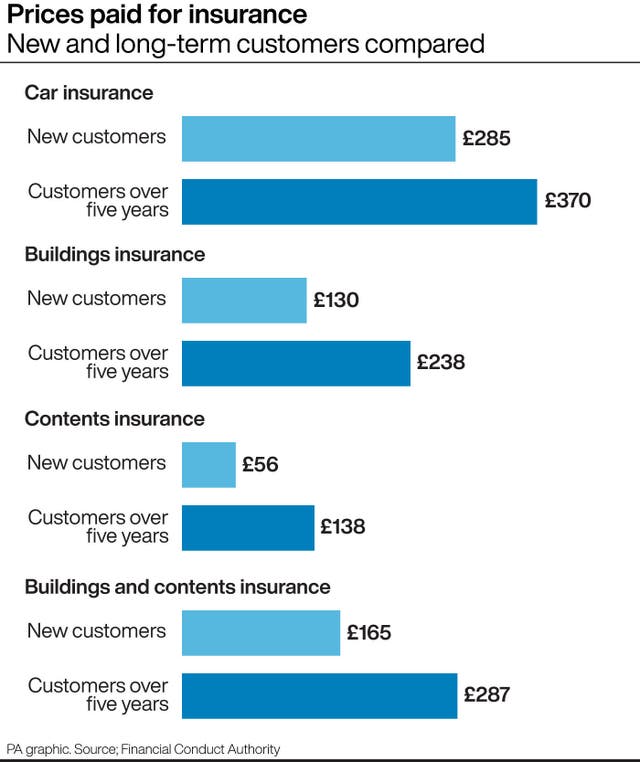

The Financial Conduct Authority has proposed that firms will not be able to charge renewing customers more than new customers.

Home and motor insurance customers should pay no more when renewing their policy than they would if they were new to their provider, under proposals by the City regulator.

It means that for existing consumers, their renewal price would be no higher than the equivalent new-business price.

However, with firms being unable to charge renewing customers more than new customers in future under the plans, it could mean the disappearance of some ultra-cheap deals from the market.

The proposals, made by the Financial Conduct Authority (FCA), would apply through the same sales channel.

For example, if the customer bought the policy online, they would be charged the same price as a new customer buying online.

Firms would be free to set new-business prices, but they would be prevented from gradually increasing the renewal price to consumers over time – known as “price walking”, other than in line with changes in a customer’s risk.

The regulator stopped short of banning auto-renewals, which could have potentially left some customers without cover.

The FCA did acknowledge that some new customers, who are currently on cheap deals, may see the prices they pay increase.

Watch: our proposals to tackle the general insurance loyalty penalty #FCAconsults #FCAfairvalue

Transcript: https://t.co/HPCkJaJhgz pic.twitter.com/Q8UE3KxIgV

— Financial Conduct Authority (@TheFCA) September 22, 2020

During a “virtual” press conference, Christopher Woolard, interim chief executive of the FCA, said: “For people who shop around, look for the best deal, there will be good deals out there in the market.

“But… at the margins there will be some people who are getting unsustainably cheap offers, often possibly offers that are designed to get them to renew year-on-year and become far more profitable customers.

“And we expect those offers to not be part of the market in the future.”

Processes such as having to wait on the phone and the accessing of information can make it harder for people to cancel contracts than it was to sign up.

Mr Woolard said: “It should be as easy to be able to cancel a renewal as it is frankly to sign up to one, that’s probably a good rule of thumb.”

Ten million policies across home and motor insurance are held by people who have been with their provider for five years or more.

The FCA previously identified six million policyholders were paying high or very high margins in 2018.

On Tuesday, it said that it estimates its proposals will save consumers £3.7 billion over 10 years overall and it will monitor their impact.

The FCA is seeking views on its proposals by January 25 2021 and the rules could come into force during the third quarter of next year.

Dame Gillian Guy, chief executive of Citizens Advice, said: “It’s nearly two years since we submitted a super-complaint on the loyalty penalty and we’re pleased to see the FCA is proposing strong action to crack down on this systematic scam.

“We’re especially happy to see it tackling price-walking – gradual year-on-year price increases – and making companies automatically switch their customers to better deals.

“It’s important to remember these are proposals and have an introduction date of late 2021 which is a long way away. It is essential that the FCA confirm and implement these quickly to potentially bring insurance customers’ prices down by £370 million a year.”

Huw Evans, director general of the Association of British Insurers (ABI), said: “The ABI agrees with the FCA that the household and motor insurance markets do not work as well as they should for all customers, and we continue to support the FCA’s work to address this.

“Insurers and brokers have already begun to tackle the issue of excessive price differences between new and existing customers through an industry initiative that has seen over 8.5 million pricing interventions across home and motor insurance worth £641 million.

“It is vital that price comparison websites and insurance brokers are subject to the same level of supervision and monitoring by the FCA to ensure a balanced approach.

“We will consider carefully this package of proposals, so that we can engage with the FCA on the most effective measures possible.

“There are winners and losers in the way the market works currently, with those who switch insurance provider every year often ending up with lower prices. The FCA has confirmed that insurers have not made excessive profits.”