Truss and Kwarteng under pressure as Bank launches emergency bond-buying action

28 September 2022, 19:34

The Bank of England stepped in to buy Government bonds after fears over the UK’s economic policies sparked a gilts sell-off.

The Bank of England has launched an emergency UK government bond-buying programme to prevent borrowing costs from spiralling out of control and stave off a “material risk to UK financial stability”.

The Bank announced it was stepping in to buy up to £65 billion worth of government bonds – known as gilts – at an “urgent pace” after fears over the Government’s economic policies sent the pound tumbling and sparked a sell-off in the gilts market.

The market turmoil had forced pension funds to sell government bonds to head off worries over their solvency, but this was threatening to see them suffer severe losses and was creating a downward spiral in gilt prices as more were offloaded.

The Bank’s extraordinary intervention, responding directly to the Government’s tax-cutting strategy, will pile further pressure on Liz Truss and Kwasi Kwarteng to defend a vision for the economy that has spooked markets and shocked most mainstream economists.

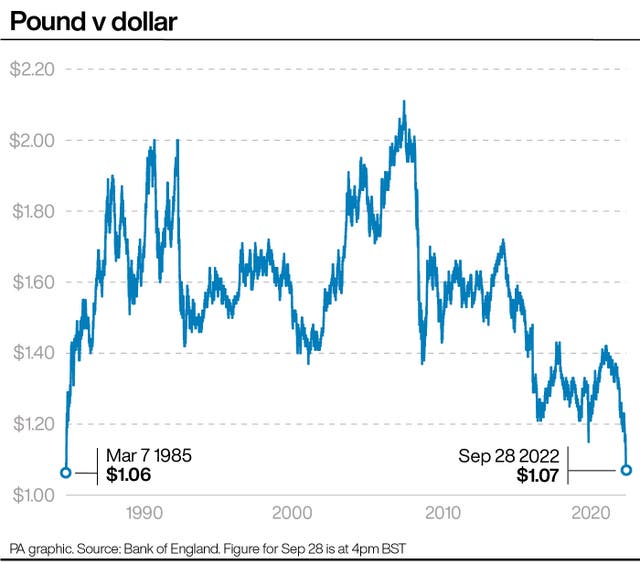

While the pound hit an all-time record low of 1.03 against the US dollar on Monday, the yield on 10-year gilts – which is a proxy for the effective interest rate on public borrowing – has also soared by the most in a five-day period since 1976, according to experts.

The scale of the crisis in the markets has led to unease in some quarters of the Tory party, while Labour has joined calls for Parliament, currently on a conference recess, to be recalled.

“The Government has clearly lost control of the economy,” Sir Keir Starmer told reporters in Liverpool.

The Labour leader said: “What the Government needs to do now is recall Parliament and abandon this budget before any more damage is done.”

However, the Financial Secretary to the Treasury Andrew Griffith insisted the Government was sticking to the plan set out by Mr Kwarteng in the Commons on Friday.

“What the Chancellor and I are focused on is delivering that economic growth plan,” he said in a pooled clip for broadcasters.

“We think they are the right plans because those plans make our economy competitive.”

In a bid to reduce future borrowing, the Government is set to ask Cabinet ministers to make efficiency savings in their departments’ existing budgets to help balance the public finances, according to the BBC.

It all comes just days before Tory MPs and thousands of members will descend upon Birmingham for Liz Truss’ first party conference as Prime Minister.

The Bank has this morning announced a gilt market operation. Full details can be found here: https://t.co/BvqFe9DZMp

— Bank of England (@bankofengland) September 28, 2022

The Bank said: “Were dysfunction in this market to continue or worsen, there would be a material risk to UK financial stability.

“This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy.

“In line with its financial stability objective, the Bank of England stands ready to restore market functioning and reduce any risks from contagion to credit conditions for UK households and businesses.”

The Treasury responded by reaffirming its commitment to the Bank of England’s independence and said the Government “will continue to work closely with the Bank in support of its financial stability and inflation objectives”.

We have agreed to indemnify the @bankofengland today in their temporary and targeted purchasing of long-dated UK government bonds to support financial stability.

We are committed to the @bankofengland 's independence, and will continue to work closely with them.

— HM Treasury (@hmtreasury) September 28, 2022

The Bank said it would buy bonds “on whatever scale is necessary” in order to steady gilts after Chancellor Mr Kwarteng’s mini-budget last Friday spooked the markets with his package of tax cuts and increased borrowing.

It said the bond-buying programme would be temporary, starting from today until October 14.

“The purpose of these purchases will be to restore orderly market conditions,” the Bank said.

It also postponed next week’s planned kick-off of its £80 billion sale of gilts under the so-called quantitative tightening programme until October 31.

It follows days of intense pressure on defined benefit pension funds, which manage savings for millions of Britons, which had been using gilts in so-called liability-driven investment (LDI) strategies that many use to protect themselves against adverse moves in inflation.

Some £1.5 trillion is invested in their LDI strategies, of which £1 trillion is invested in bonds, and pension funds have been racing to sell gilts to meet calls for more collateral, but this has been forcing the already tumbling price of gilts lower.

The Bank’s action comes as Neither Mr Kwarteng nor Ms Truss have shown any willingness to step back from the policies announced on Friday, many of which made good on the promises she had delivered on her leadership campaign trail over the summer.

But the market angst in recent days has seen the Chancellor step up efforts to reassure the City about his economic plans after the International Monetary Fund (IMF) criticised the Government’s strategy.

At a meeting on Wednesday, Mr Kwarteng “underlined the government’s clear commitment to fiscal discipline” at a meeting with Bank of America, JP Morgan, Standard Chartered, Citi, UBS, Morgan Stanley and Bloomberg amongst others.

He also told the meeting that the plan announced on Friday would “expand the supply side of the economy through tax incentives and reforms, helping to deliver greater opportunities and bear down on inflation”, according to a Treasury readout.

Mortgage borrowers have also been hit by a record overnight drop in the choice of home loan products as the economic fallout from Friday’s mini-budget continues.

The Bank has been facing calls to convene an emergency meeting to consider hiking interest rates to try and counter the Government’s tax cut measures.

The Bank’s chief economist, Huw Pill, said on Tuesday a “significant monetary response” may be required, but signalled this would not come until policymakers are due to meet as scheduled in November.

Representatives from Bank of America, JP Morgan, Standard Chartered, Citi, UBS, Morgan Stanley and Bloomberg were called to attend a meeting with Mr Kwarteng on Wednesday following days of turmoil.

In an extraordinary statement, the IMF said it was “closely monitoring” developments in the UK and was in touch with the authorities, urging the Chancellor to “re-evaluate the tax measures”.

It warned the current plans, including the abolition of the 45p rate of income tax for people on more than £150,000, are likely to increase inequality.