Political instability sees UK economic outlook downgraded by ratings agency

22 October 2022, 07:04

Moody’s said the change in outlook was driven by ‘heightened unpredictability in policymaking’.

The UK’s economic outlook has been downgraded from “stable” to “negative” by the ratings agency Moody’s due to political instability and high inflation.

In a report published on Friday night, Moody’s said the change in outlook was driven by “heightened unpredictability in policymaking amid weaker growth prospects and high inflation” and “risks to the UK’s debt affordability from likely higher borrowing and risk of a sustained weakening in policy credibility”.

Rating agencies rate a country on the strength of its economy and provide governments with a score based on the likelihood that they will be able to pay back debt.

The rating affects how much it costs governments to borrow money in the international financial markets.

British retail sales volumes fell 1.4% in September, according to today’s Office for National Statistics estimate. Moody’s Richard Etheridge comments on the latest figures, consumers and the grocery sector. 👉 Read our analysis on European consumers: https://t.co/vdUyhQhTnB pic.twitter.com/VNMqJ59InY

— Moody's Investors Service (@MoodysInvSvc) October 21, 2022

According to the agency, an outlook period “typically lasts 12-18 months”.

However, while the UK’s economic outlook has been graded as “negative”, Moody’s credit rating for the UK remains unchanged at Aa3.

The agency said this rating reflects the UK’s economic resilience “despite the weakening in fiscal policy predictability in recent years”.

It added: “The country’s long-standing institutional framework remains strong and will continue to support the UK’s ability to respond to shocks, as seen during the pandemic. Furthermore, the structure of the UK government debt, with a very long average maturity of around 15 years, as well as a deep domestic investor base adds a degree of resilience to the credit profile in the face of shocks.

“The UK’s local and foreign currency country ceilings remain unchanged at Aaa. The three-notch gap between the local currency ceiling and the sovereign rating is driven by the government’s relatively small footprint in the economy, a fairly robust external payments position and a diversified economy.”

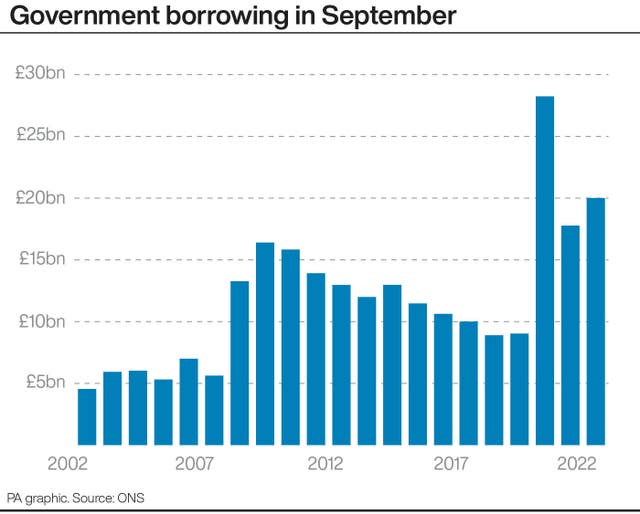

It comes as Chancellor Jeremy Hunt vowed to do “whatever necessary” to drag government debt lower after official figures revealed that borrowing swelled to £20 billion in September.

The Office for National Statistics (ONS) reported that a jump in debt interest grew borrowing beyond the expectations of economists, laying bare the challenge facing the Chancellor and new prime minister ahead of the fiscal event at the end of this month.

The latest reading for borrowing, excluding state-owned banks, marked the second-highest September on record, only surpassed during the height of the Covid-19 pandemic, the ONS said.

Borrowing in September outpaced the predictions of economists, who had forecast £17 billion for the month, and was significantly above the £14.8 billion estimated by the Office for Budget Responsibility (OBR) back in March.

Mr Hunt said: “Strong public finances are the foundation of a strong economy.

“To stabilise markets, I’ve been clear that protecting our public finances means difficult decisions lie ahead.

“We will do whatever is necessary to drive down debt in the medium term and to ensure that taxpayers’ money is well spent, putting the public finances on a sustainable path as we grow the economy.”

The recently appointed Chancellor has already reversed a number of key financial policies announced last month by predecessor Kwasi Kwarteng, including plans to scrap the increase in corporation tax to 25%.

The latest ONS data revealed that increased borrowing was driven by £7.7 billion of debt interest payments for the month, reflecting an increase of £2.5 billion compared with the same month in 2021.

It was the highest September interest figure since records began in 1997.

Significantly higher debt interest payments linked to Retail Prices Index (RPI) inflation drove the increase, the ONS said.