Hunt sets out tax rises and spending cuts in the face of economic storm

17 November 2022, 12:14

Chancellor Jeremy Hunt was setting out a package of £30 billion of spending cuts and £24 billion in tax rises over the next five years.

Jeremy Hunt promised to “tackle the cost-of-living crisis” and “rebuild our economy” as he set out plans for tax rises and spending cuts.

The Chancellor said there would be a “shallower downturn” as a result of his measures but the Office for Budget Responsibility (OBR) believed the economy was “now in recession”.

He told MPs his three priorities were “stability, growth and public services”, as he delivered his autumn statement.

The OBR forecast the UK economy would shrink by 1.4% next year, Mr Hunt said.

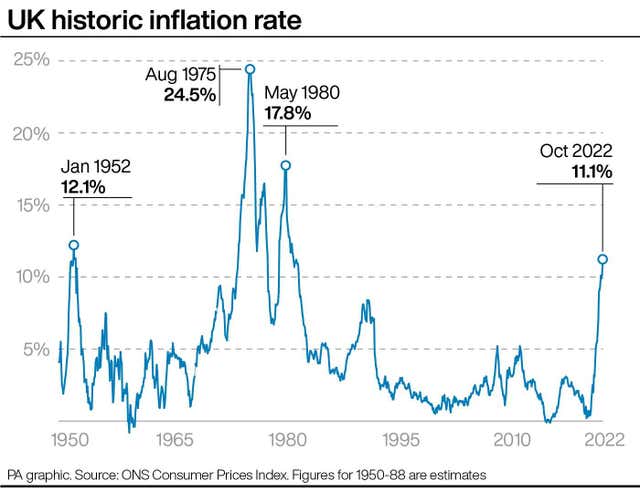

“The OBR forecast the UK’s inflation rate to be 9.1% this year and 7.4% next year,” he said.

“They confirm that our actions today help inflation to fall sharply from the middle of next year.

“They also judge that the UK, like other countries, is now in recession. Overall this year, the economy is still forecast to grow by 4.2%.

“GDP (gross domestic product) then falls in 2023 by 1.4%, before rising by 1.3%, 2.6%, and 2.7% in the following three years.

“The OBR says higher energy prices explain the majority of the downward revision in cumulative growth since March.

“They also expect a rise in unemployment from 3.6% today to 4.9% in 2024 before falling to 4.1%.”

Mr Hunt was setting out a package of £30 billion of spending cuts and £24 billion in tax rises over the next five years.

His package is in stark contrast to his predecessor Kwasi Kwarteng’s ill-fated plan for £45 billion of tax cuts, less than two months ago, which spooked the markets, pushed up the cost of borrowing and contributed to the downfall of Liz Truss’ short-lived administration.

Mr Hunt said: “I understand the motivation of my predecessor’s mini-budget and he was correct to identify growth as a priority. But unfunded tax cuts are as risky as unfunded spending.”

Mr Hunt said repairing the nation’s finances involved “taking difficult decisions”.

He told MPs: “Anyone who says there are easy answers is not being straight with the British people: some argue for spending cuts, but that would not be compatible with high-quality public services.

“Others say savings should be found by increasing taxes, but Conservatives know that high tax economies damage enterprise and erode freedom.

“We want low taxes and sound money. But sound money has to come first because inflation eats away at the pound in people’s pockets even more insidiously than taxes.

“So, with just under half of the £55 billion consolidation coming from tax, and just over half from spending, this is a balanced plan for stability.”

He announced:

– The threshold at which the 45p top rate of income tax is paid will be reduced from £150,000 to £125,140, although different rates apply in Scotland.

– The income tax personal allowance, higher rate threshold, main national insurance thresholds and the inheritance tax thresholds will be frozen until April 2028, something which will result in more people paying more tax as a result of “fiscal drag” as wages increase.

– The windfall tax on oil and gas giants will increase from 25% to 35% and a 45% levy on electricity generators will help raise an estimated £14 billion next year.

– Tax-free allowance for capital gains will reduce in 2023-24 from £12,300 to £6,000 and again to £3,000 in 2024-25.

– Electric vehicles will no longer be exempt from vehicle excise duty from April 2025, to make the motoring tax system “fairer”.

– Government spending will continue to increase in real terms every year for the next five years, but at a slower rate than previously planned.

– Stamp duty cuts announced in Mr Kwarteng’s mini-budget will now be time-limited, ending on March 31 2025.

– The Government would protect the increases in departmental budgets already set out in cash terms for the next two years, meaning real-terms cuts due to inflation and pressure on public sector wages.

– The defence budget will keep meeting the Nato target of 2% of GDP but the overseas aid budget will not be returned to its goal of 0.7% of national income “until the fiscal system allows”.

– An extra £2.3 billion per year will be invested in schools in England over the next two years.

– The implementation of social care reforms will be delayed for two years.

– The NHS budget in England will increase by an extra £3.3 billion in each of the next two years.